Bank Reconciliation Statement - Class 10 Elements Of Book Keeping And Accountancy - Extra Questions

On 1st January 2010, Rakesh had an overdraft of Rs 8,000 as showed by his cash book. Cheques amounting to Rs. 2,000 had been paid in by him but were not collected by the bank in January 1, 2010. He issued cheques of Rs.800 which were to presented to the bank for payment up to that day. There was a debit om his pass book of Rs. 60 for interest and Rs. 100 for bank charges.

Prepare bank reconciliation statement for comparing both the balance.

Prepare bank reconciliation statement for comparing both the balance.

From the following particulars,prepare a bank reconciliation statement as at March 31, 2010.

i) Balance as per cash book,Rs.3,200.

ii) Cheque issued but not presented for payment, Rs.1,800.

iii) Cheque deposited but not collected upto March 31, 2010,Rs. 2,000.

iv) Bank charges debited by bank, Rs. 150.

Prepare bank reconciliation statement.

i) Overdraft shown as per cash book on December 31, 2010 Rs. 10,000.

ii) Bank charges for the above period also debited in the pass book Rs. 100.

iii) Interest on overdraft for six months ending December 31, 2010, Rs. 380 debited in the pass book.

iv) issued but not incashed prior to December 31, 2010 amounted to Rs. 2,150.

v) Interest on Investment collected by the bank and credited in the pass book, Rs. 600.

vi) Cheques paid into bank but not cleared before December, 31 2010 were Rs. 1,100.

Bank balance of Rs.40,000 showed by the cash book of Atul on December 31,2010.It was found that three cheques of Rs.2,000, Rs.5,000 and Rs.8,000 deposited during the month of December were not credited in the pass book till January 2,Two cheques of Rs. 7,000 and Rs,8,000 issued on December 28, were not presented for payment, till January 3, 2010.In addition to it bank had credited Atul for Rs.325 as interest and had debited him with Rs. 50 as bank charges for which there were no corresponding entries in the cash book.

Prepare a bank reconciliation statement as on December 31, 2010.

Balance as per pass book of Mr Kumar is 3,000.

i) Cheque paid into bank but not yet cleared Ram Kumar Rs 1000 & Kishore Kumar Rs 500.

ii) Bank Charges Rs.300

iii) Cheque issued but not presented Hameed Rs 2,000 & Kapoor Rs 500.

iv) Interest entered in the pass book but not entered in the cash book Rs 100.

Prepare Bank reconciliation statement.

On March 31,2010, the cash showed a balance of Rs.3,700 as cash at bank, but the bank pass book made up to same date showed that cheques for Rs. 700, Rs. 300, and Rs. 180 respectively had not presented for payment.Also, cheque amounting to Rs. 1,200 deposited into the account had not been credited.Prepare a bank reconciliation statement.

Prepare bank reconciliation statement of Shri Bhandari as on December 31, 2010

i) The payment of a cheque for Rs.550 was recorded twice in the pass book.

ii) Withdrawal column of the pass book under cast by Rs.200.

iii) A Cheque of Rs.200 has been debited in the bank column of the cash book but it was not sent to bank at all.

iv) A cheque of Rs.300 debited to bank column of the pass book was not sent to the bank.

v) Rs. 500 in respect of dishonored cheque were entered in the pass book but not in the cash book.

Overdraft as per pass book is Rs. 20,000.

What is a bank overdraft ?

Prepare Bank reconciliation statement as on December 31,On this day, the pass book of Mr. Himanshu showed a balance of Rs. 7,000.

i) Cgeque of Rs.1,00 directly deposited by a customer.

ii) The bank has credited Mr. Himanshu for Rs. 700 as interest.

iii) Cheques for Rs. 3000 were issued during the month of December but of these cheques for Rs.1,000 were not presented during the month of December.

Give one word or term or phrase which can substitute each of the following statement.

Statement showing the causes of disagreement between the balance of Cash Book and Pass book.

Give one word or term or phrase which can substitute each of the following statement.

A statement which is prepared so as to agree the bank balance as shown by the pass book with the bank balance as shown by the bank column of the cash book.

What is Bank Reconciliation Statement?

Raghav & Co have two bank accounts,Account No.I and Account No.II. From the following particulars relating to Account No.I, find out the balance on that account of December 31, 2010 according to the cash book of the firm.

i) Cheques paid into bank prior to December 31, 2010, but not credited for Rs. 10,000.

ii) Transfer of funds from Account No II to Account No I recorded by the bank, on December 31, 2010 but entered in the cash book after hat date for Rs.8,000.

iii) Cheques issued prior to December 31, 2010 but not presented until after that date for Rs. 7,429

iv) Bank charges debited by bank not entered in the cash book for Rs. 200.

v) Interest debited by the bank not entered in the cash book, Rs. 580.

vi) Overdraft as per pass book,Rs.18,990.

Prepare a bank reconciliation statement from the following particulars and show the balance as per cash book

i) Balance as per pass book on December 31, 2010 overdrawn Rs.20,000.

ii) Interest on bank overdraft not entered in the cash book Rs.2,000.

iii) Rs.200 insurance premium paid by bank has not been entered in the cash book.

iv) Cheques drawn in the last week of December,2010, but not cleared till date for Rs.3,000 and Rs.3,500.

v) Cheques deposited into bank on November, 2010 , but yet to be credited on dated December 31, 2010, Rs.6,000.

vi) Wrongly debited by bank,Rs.500.

Who prepares a Bank Reconciliation Statement?

Overdraft shown by the pass book of Mr. Murli is Rs. 20,Prepare bank reconciliation statement on dated December 31, 2010.

i) Bank charges debited as per pass book, Rs. 500

ii) Cheques recorded in the cash book but not sent to the bank for collection, Rs.2,500.

iii) Received a payment directly from customer, Rs. 4,600.

iv) Cheque issued but not presented for payment. Rs. 6,980.

v) Interest credited by the bank, Rs.100.

vi) LIC paid by bank, Rs.2,500.

vii) Cheques deposited with the bank but not collected, Rs. 3,500.

Prepare a bank reconciliation statement from the following particulars as on $$31^{st}$$ March, $$2018$$.

| Particulars | (Rs.) |

| Debit balance as per bank column of the cash book | $$18,60,000$$ |

| Cheque issued to creditors but not yet presented to the Bank for payment | $$3,60,000$$ |

| Dividend received by the bank but not entered in the Cash book | $$2,50,000$$ |

| Interest allowed by the Bank | $$6,250$$ |

| Cheques deposited into bank for collection but not collected by bank up to this date | $$7,70,000$$ |

| Bank charges not entered in Cash book | $$1,000$$ |

| A cheque deposited into bank was dishonoured, but no intimation received | $$1,60,000$$ |

| Bank paid house tax on our behalf, but no intimation received form bank in this connection | $$1,75,000$$ |

On $$31-3-2020$$, Mahesh's Cash Book Showed a Bank overdraft of $$Rs. 98,700$$. On comparison he find the following:

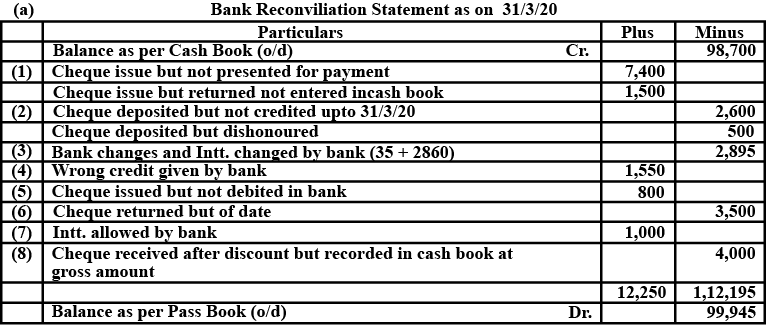

$$(1)$$ Out of the total cheques of $$Rs. 8,900$$ issued on $$27^{th}$$ March, one cheque of $$Rs. 7,400$$ was presented for payment on $$4^{th}$$ April and the other cheque of $$Rs.1,500$$ handed over to the customer, was returned by him and in lieu of that a new cheque of the same amount was issued to him on $$1^{st}$$ April. No entry for the return was made.

$$(2)$$ Out of total cash and cheques of $$Rs. 6,800$$ deposited in the Bank on $$24^{th}$$ March, one cheque of $$Rs. 2,600$$ was cleared on $$3^{rd}$$ April and the other cheque of $$Rs. 500$$ was returned dishonoured by the bank on $$4^{th}$$ April.

$$(3)$$ Bank charges $$Rs. 35$$ and Bank interest $$Rs. 2,860$$ charged by the bank appearing in the passbook are not yet recorded in the cash book.

$$(4) $$ A cheque deposited in his another account of $$Rs. 1,550$$ wrongly credited to this account by the bank.

$$(5)$$ A cheque of $$Rs. 800$$, drawn on this account, was wrongly debited in another account by the bank.

$$(6)$$ A debit of $$Rs. 3,500$$ appearing in the bank statement for an unpaid cheque returned for being 'out of date' had been re-dated and

deposited in the bank account again on $$5^{th}$$ April $$2020$$.

$$(7)$$ The bank allowed interest on deposit $$Rs. 1,000$$

$$(8)$$ A customer who received a cash discount of $$4\%$$ on his account of $$Rs. 1,00,000$$ paid on a cheque on $$20^{th}$$ March $$2020$$. The easier erroneously entered the gross amount in the bank column of the Cash Book.

Prepare Bank Reconciliation Statement as on $$31-3-2020$$